FAQ's:

DEFINITION

OF TERMS:

Accrual

Method |

- |

A

method for the valuation

of fixed income funds

which calculates Net

Asset Value (NAV) using

the assets’ purchase

or cost price. Returns

on the Fund are from

the amortization of

the bond cost and the

accrual of interest

on the securities comprising

the portfolio. This

method disregards changes

in the prices of the

underlying securities.

The accrual method is

distinguished from the

marked to market method

which values the fund’s

securities at the current

market price. |

Active

Management |

- |

Refers

to a style of investment

management that seeks

to attain returns above

a set benchmark or standard

by making more active

adjustments to the various

types of assets and

securities within an

asset class to take

advantage of expected

price movements. This

is compared to a more

passive type of management

where a “buy-and-hold

strategy” is employed

or where the fund manager

buys assets that seeks

to mirror the composition

and return of a desired

benchmark. |

Annualized

Return |

- |

The

value that an investment

has achieved over a

12-month period. |

Bond |

- |

A

certificate of indebtedness

issued by a corporation

or government, with

a stated interest rate

and fixed due dates

when interest and principal

must be paid. |

Coupon |

- |

The

current interest rate

for a fixed income security. |

Cut-off

time |

- |

The

latest time by which

subscriptions or redemptions

to a fund utilize the

applicable NAVPU. Subscriptions

or redemptions after

the cut-off time will

acquire the NAVPU of

the next applicable

banking day. |

Duration |

- |

Also

known as Macaulay duration,

is the weighted average

time to receipt of the

present value of the

cashflows from a bond.

This is a tool used

to determine the risk

in a bond (see Modified

Duration). |

Early

Redemption Penalty |

- |

This

is the extra cost charged

to the investor for

redeeming units of a

fund before the Minimum

Holding Period has elapsed. |

Equity |

- |

Considered

as a one of the general

asset classes in an

investment portfolio,

distinguished from fixed

income assets. Equity

represents ownership

in a corporation, and

represents a claim on

the proportionate share

of the corporation’s

assets and profits. |

Explanatory

Memorandum |

- |

Document

which contains the summary

of the UITF’s

Plan Rules and Regulations,

and the terms and conditions

governing the investments

of the UITFs. |

Fixed

Income |

- |

One

of the general asset

classes in an investment

portfolio, distinguished

from equities. Fixed

Income securities have

a stated return and

maturity value. Examples

of fixed income assets

are bonds, loans, and

deposits. |

Fund

Manager |

- |

The

person or entity responsible

for determining the

composition, changes,

and movements of the

fund’s portfolio,

in order to optimize

fund performance while

controlling the risk

of the portfolio. |

Fund

Structure |

- |

Refers

to the regulatory structure

that governs the investment

fund. In the Philippines,

there are currently

3 types of fund structures,

mutual funds, common

trust funds (CTF) and

unit investment trust

funds (UITF). |

Fundamental

Analysis |

- |

Is

a method used to determine

the value of a financial

instrument by analyzing

the economic, political,

environmental and other

relevant factors affecting

the supply and demand

for that instrument.

For equity investments,

the company’s

financial situation,

business prospects and

profitability are some

of the factors analyzed.

For fixed income investments,

the credit risk of the

issuer and its yield

relative to market interest

rates are studied. Fundamental

analysis is contrasted

from technical analysis

which focuses on analyzing

price movements by identifying

price chart patterns. |

Index |

- |

An

index is a collection

of selected securities

which is used as a representation

of the general characteristics

and performance of a

particular market. |

Investment

Grade |

- |

Refers

to bonds judged likely

to meet payment obligations

which are deemed suitable

for conservative investors.

These bonds have ratings

of at least Baa3 from

Moody’s or at

least BBB- from Standard

& Poor’s. |

Launch

Date |

- |

The

specific date wherein

a new product is introduced

to the public. |

Marked-to-Market

(MTM) method |

- |

A

vauation method where

assets of the Fund are

valued at the current

market price, taking

into account unrealized

capital gains or losses.

This is the international

standard used to value

the assets of both equity

and fixed-income funds. |

Maturity |

- |

The

date on which a loan,

bond, mortgage, or other

debt or security is

due to be repaid. |

Minimum

Additional Participation

Amount |

- |

This

is the smallest additional

amount an existing investor

can invest into the

fund. |

Minimum

Holding Period |

- |

The

minimum number of days

that an investor must

keep his investment

in the fund before he

can redeem it without

penalty. |

Minimum

Participation Amount |

- |

This

is the smallest amount

which must be invested

in a fund. |

Minimum

Redemption Amount |

- |

This

is the smallest amount

that an investor can

redeem out of his investment

in a fund. |

Modified

Duration |

- |

This

is an estimate of how

the price of a bond

will change for a given

change in yield. The

higher the modified

duration of a security,

the higher its price

sensitivity to interest

rate movements. |

Money

Market Instrument |

- |

Fixed

income security with

a maturity of less than

one year. |

Mutual

Fund |

- |

A

Mutual Fund is an investment

vehicle managed by an

Investment Company (IC)

that pools money of

shareholders in the

Fund. The money is invested

in a single portfolio

comprised of stocks,

bonds, and other securities. |

Net

Asset Value (NAV) |

- |

The

net worth of the assets

of a Fund. NAV is calculated

by subtracting the Management

Fee of the Fund plus

other Expenses and Liabilities,

from the Total Asset

Value, which is the

current market value

of all the securities

and holdings that comprise

the Fund Portfolio.

NAV = Total Asset Value

– (Management

Fee + Other Expenses

and Liabilities) |

Net

Asset Value Per Share |

- |

The

current worth of a Share

in a Mutual Fund. NAVPS

is computed by dividing

the current NAV of a

Fund by the total number

of Units of Participation

held by investors. |

Net

Asset Value Per Unit |

- |

The

current worth of a Unit

of Participation in

a Unit Investment Trust

Fund (UITF). NAVPU is

computed by dividing

the current NAV of a

Fund by the total number

of Units of Participation

held by investors. |

Passive

Management |

- |

Refers

to a style of investment

management that seeks

to achieve performance

equal to the market

or index returns. |

Portfolio |

- |

An

investor's collection

of investment holdings,

usually with reference

to its composition.

It may be a mix of different

classes of securities,

such as bonds, property,

shares, and cash. |

Redemption |

- |

The

process of selling back

one’s Units of

Participation/Shares

in the Fund. This is

done at the applicable

NAVPU / NAVPS on the

day the Redemption Order

is submitted by the

Investor. The order

must be received by

the Trustee on or before

the Cut off Time for

the day; otherwise,

the transaction will

be processed on the

next banking day. |

Redemption

Notice Period |

- |

Redemption

Notice Period refers

to the number of days

after redemption before

the proceeds are given

to the investor. For

instance, if the redemption

notice period for a

Fund is 4 banking days,

this means that if the

client redeems by the

redemption cut-off time

today (Trade Date),

the redemption proceeds

will be given to the

investor on the fourth

banking day from now,

counting today (Trade

Date + 3). |

Reserves |

- |

Also

known as legal reserves,

it is a percentage of

the value of Common

Trust Funds (CTFs) that

must be set aside for

liquidity purposes,

as mandated by the Bangko

Sentral ng Pilipinas.

Unit Investment Trust

Funds (UITFs) have no

legal reserve requirement. |

Return |

- |

The

sum of interest, principal

payments, reinvestment

income, and any realized

and unrealized capital

gains or losses expressed

as a percentage of principal

in annual terms. |

Risk |

- |

The

possibility of loss

on an investment. Investments

with greater risk must

provide higher expected

returns to be attractive

to investors. |

Risk

Management |

- |

The

process of monitoring

and controlling various

risk factors in an investment

portfolio to ensure

that there are no unwanted

or unintended risks

in the portfolio that

could cause performance

surprises. |

Stocks |

- |

Also

known as shares of a

company, it is a certification

of ownership of a fraction

of the company. These

are the specific securities

traded in the equity

markets. |

Subscription |

- |

The

process by which Units

of Participation of

a Fund are purchased. |

Technical

Analysis |

- |

It

is an approach to the

analysis of price movements

of financial instruments

and their future trends.

It examines the technical

factors of market activity,

often represented by

charting patterns, as

contrasted with fundamental

analysis. Technical

analysts normally examine

patterns of price change,

rates of change, and

changes in volume of

transactions, in the

hope of being able to

predict and profit from

expected future trends. |

Trustee |

- |

The

entity authorized to

hold the assets of a

fund for the benefit

of the beneficiaries

or participants. |

Unit

Investment Trust Fund

(UITF) |

- |

Is

a trust product that

pools the money of various

investors into a single

portfolio managed by

a professional investments

team. The UITF allows

the investor to own

participation in a diversified

portfolio of stocks

or bonds through ownership

in units of the fund. |

Valuation

of the fund |

- |

This

refers to the method

used in order to calculate

the Net Asset Value

of the securities. The

two commonly practiced

methods are the Accrual

Method and the Marked-to-market

method. |

Volatility |

- |

It

is how much variability

there is in the price

changes of the investment.

The more variability

there is, the higher

the volatility. |

Yield

to Maturity |

- |

The

percentage rate of return

earned on a fixed income

security assuming it

is held to its maturity

date. It assumes that

coupon interest paid

over the life of the

security is reinvested

at the same rate. |

| Q. |

What

is a fund? |

| A. |

A

fund, also known as an

investment fund, is a

collection of stocks,

bonds or other securities

owned by a group of investors

and managed by a professional

investment company. |

| |

|

| Q. |

What

is a UITF? |

| A. |

Similar

to a Common Trust Fund

(CTF), a Unit Investment

Trust Fund (UITF) is a

trust product that pools

the money of various investors

into a single portfolio

managed by a professional

investments team of a

trust department of a

bank or an institution

with a trust license.

The Fund allows the investor

to own participation in

stocks or bonds at a fraction

of the costs and minimum

investment amounts usually

associated with these

investments. Moreover,

the investor need not

track his investment daily,

nor worry about what stocks

or bonds to buy or sell.

This is because skilled

fund managers with years

of asset management experience

handle the portfolio day-in,

day-out. But unlike the

CTF, a UITF must be valued

using the marked-to-market

method and is not required

to keep any reserves with

the Bangko Sentral ng

Pilipinas. |

| |

|

| Q. |

What

is a Mutual Fund? |

| A. |

A

Mutual Fund is an investment

vehicle managed by an

Investment Company (IC)

that pools money of shareholders

in the Fund. The money

is invested in a single

portfolio comprised of

stocks, bonds, and other

securities. |

| |

|

| Q. |

What

are the differences between

a Mutual Fund and a UITF? |

| A. |

| |

UITF |

Mutual

Fund |

Management |

The Trust Department

of a Bank |

Investment

Company |

Participation |

Units of Participation |

Shares

in the mutual Fund

Company |

Regulator |

BSP |

SEC |

Valuation

Method |

MTM |

Accrual

or MTM |

Reserves |

None |

None,

but requires IC

P50 M paid-up capital |

Taxes |

None |

Doc

Stamps of P1 per

P200 par value |

Sales

License |

Standardized

training from TOAP-accredited

trainor |

Agents

need SEC license

to sell Fund |

|

| |

|

| Q. |

Why

should I invest in a fund? |

| A. |

There

are several reasons why

it would be wise to invest

in a fund rather than in

securities directly.

• |

Professionally Managed:

The fund is constantly

monitored by a team

of professional

investors, making

adjustments in order

to seek out the

fund's best possible

performance. Not

only is the investor

relieved of the

burden of constantly

researching and

monitoring the securities,

but also, this responsibility

falls on a fund

manager or a team

whose full time

job is to manage

the fund. These

managers come with

a wealth of training

and experience under

their belts. |

• |

Diversification:

A fund is typically

invested in hundreds

or even thousands

of different securities.

No more than 10%

of its assets can

be invested in a

single security,

except for government

securities. This

diversification

spreads the risks

over a broad base

thereby limiting

potential loss. |

• |

Affordability: A

fund pools together

the resources of

many small investors

so as to create

greater buying power

than they could

achieve by themselves.

In addition, economies

of scale come in

because funds purchase

large volumes of

a specific security

and thus, are able

to spread some of

the costs like commissions

and processing fees

over many investors.

In essence, an investor

is buying shares

or units of participation

in the fund. Also,

funds allow investors

to gradually add to their investments

over time. |

• |

Liquidity: Also,

a fund gives investors

greater liquidity

than do stocks or

bond. You can purchase

or redeem your shares

on any business

day. |

|

| |

|

| Q. |

What

are the risks involved in

investing? |

| A. |

| A. |

Market

risk |

- |

is the danger associated

with unpredictable

events that influence

the performance

of the entire market.

Examples of this

include economic

recessions, natural

calamities, and

political scandals.

This type of risk

cannot be diversified

out of an investment

portfolio, for it

affects most or

all securities in

the market. |

| B. |

Credit

risk |

- |

refers to the possibility

a debtor will default

on a loan. This

non-payment of the

principal usually

happens in fixed-income

instruments. Investing

in bonds with a

high credit rating

minimizes this risk;

keeping a portfolio

well-diversified

also helps. |

| C. |

Value

of the fund may

go up or down |

- |

Returns and performance

of the fund are

not guaranteed,

therefore the investment

is subject to possible

loss of principal.

Even if the Unit

Trust Fund has provided

high returns in

the past, historical

performance of the

Fund is no guarantee

of its future performance. |

| D. |

Not

covered by the PDIC |

- |

Unlike Bank Deposits,

which are insured

up to P250,000 by

the Philippine Deposit

Insurance Commission

(PDIC), an investment

in a UITF is uninsured.

This is because

investment in the

UITF is not considered

a deposit with the

Bank. |

|

| |

|

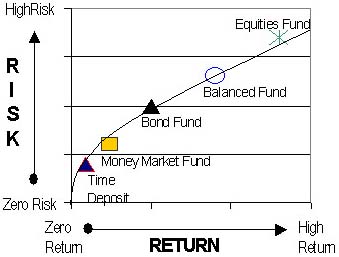

| Q. |

How

is the fund's risk and return

determined? |

| A. |

The

risk and return of the

Fund is determined in

large part by the asset

type or types that comprise

it. To illustrate, the

graph to the right plots

the quantified risk and

return characteristics

of the various types of

Funds over a span of five

years. Portfolios invested

purely in cash or time

deposits would generally

have the least exposure

to risk, as well as the

least return. On the other

end of the spectrum, portfolios

with holdings composed

entirely of equities is

high-risk, yet high return.

A curve called the risk-return

frontier may be used to

approximate the trade-off

between risk and return. |

| |

|

| Q. |

What

are the different kinds

of investment funds? What

are their differences? |

| A. |

| A. |

Money

Market Fund |

- |

These funds invest

in short-term debt

securities, which

are fixed income

instruments with

remaining lifetime

of less than a year.

Such securities

a generally stable

asset valuation

given that they

are close to maturity.

The return objective

of these low risk,

low return funds

is usually to perform

better than the

short-term time

deposit rates in

the market. |

| B. |

Equity

Fund |

- |

These funds are

invested in stocks.

Stocks are shares

of ownership in

a company issued

for the purpose

of raising capital.

They have a tendency

to be volatile,

with valuations

changing considerably

along with company

developments and

market events. However,

the returns on these

investments, comprised

of both dividends

and capital gains,

are consistently

high in the long

run. Equity funds

aim to achieve capital

growth over a long

period of time.

These funds provide the potential for

high returns but

with it comes more

volatility or risk. |

| C. |

Fixed

Income (Bond) Funds |

- |

These funds are

invested in fixed

income instruments.

Issued by governments

and corporations

to borrow capital,

they are called

"fixed income"

because they are

obligations to repay

fixed amounts of

interest, plus the

principal, in the

future. Since the

interest returns

on these instruments

are preset, these

securities are less

risky than stocks.

These funds are

conservatively managed

than equity funds,

and are less subject

to variability in

returns. The objective

is often to preserve

capital while producing

a moderate income

by investing in

medium to long-term

bonds or fixed income

securities issued

by the government

or corporations. |

| D. |

Balanced

Fund |

- |

are invested in

a mix of equities

and debt. They combine

the growth potential

of higher-risk stocks

with the less volatile

returns of fixed-income

securities. Their

risk-return characteristics

fall between Equity

Funds and Fixed-Income

Funds. |

|

| |

|

| Q. |

What

are open-end and closed-end

funds? |

| A. |

Open-end funds sell as

many units as investors

are willing to buy. This

makes the fund grow bigger

as every new investor

buys a unit of the fund.

Closed-end funds sell

only a fixed number of

shares. After that, the

shares are traded on an

exchange. |

| |

|

| Q. |

What

type of fund is best for

an investor? |

| A. |

Different types of funds

have different objectives.

So an investor should

choose the fund which

satisfies his own needs

or preferences.

a. Investment

Objective

• |

Capital Growth -

some funds are focused

on giving higher

returns. These funds

are typically riskier

than capital preservation

funds. |

• |

Capital Preservation

- some funds are

aimed at maintaining

the investor's invested

capital, usually

offering smaller

returns at a lower

risk. |

b. Time horizon

• |

Another key characteristic

would be how long

the investor can

afford to leave

his money untouched

in the investment.

This affects considerably

how much risk or

volatility the investor

can handle. Generally,

the longer the acceptable

time horizon, the

greater the tolerance

for risk. |

c. Risk profile

• |

Risk-seeker - the

investor prefers

investment instruments

with high returns

even if these vary

wildly from period

to period. |

• |

Risk-averse - the

investor may opt

for stable, predictable

performance despite

returns that are

generally lower. |

Example:

An investor wishes to

build a vacation house

for his retirement in

ten years. He can afford

to keep the money allotted

for this locked up for

the entire period, and

he can tolerate up to

moderate risk if his money

can appreciate considerably.

Given these characteristics,

he may want a fund that

delivers capital growth.

Towards

this objective, he may

prefer an equity fund.

Equities provide generally

higher growth over debt

instruments, in exchange

for a higher risk exposure.

However, even as they

are more volatile than

other instruments, returns

on equities tend to average

out in the long-term.

An investor willing to

wait out a ten to fifteen

year time frame will have

the advantage of a greater

probability of high returns

at low level of risk. |

| |

|

| Q. |

How

do you invest in a fund? |

| A. |

In order to invest in

a fund, a person must

buy shares or units of

participation in the fund.

The value of one unit

can be calculated by dividing

the current market value

of the entire fund by

the number of outstanding

units. The market value

of the entire fund is

equal to the market value

of all the securities

in the fund. This is known

as Net Asset Value or

NAV. By dividing the NAV

by the number of outstanding

units, we get the NAV

per unit of participation

or NAVPU. The NAVPU is

the price the investor

must pay for one share

or unit of participation.

NAVPU = Total Assets

of the Fund - (Management

Fee + Other Expenses and

Liabilities)

Outstanding

Number of Units of the

Fund |

| |

|

| Q. |

When

are Net Asset Values calculated?

Would I know my Net Asset

Value per Share/Unit before

I invest? |

| A. |

The fund's Net Asset Value

per Unit/Share is calculated

at the end of the day.

This means that if an

investor is able to buy

into the fund before the

cut-off time for the day,

he will only find out

his Net Asset Value per

Unit/Share the following

day. |

| |

|

| Q. |

How

is the fund valued? |

| A. |

There are two ways to value

fixed income funds, the

accrual method and the marked-to-market

method.

In

the accrual method the

value of each asset in

the Fund is recorded at

its purchase price and

coupon payments are accrued

or accumulated on a daily

basis(less tax expenses).

Take note that this does

not reflect the actual

market prices at which

assets in the Fund can

be traded.

On

the other hand, the marked-to-market

method values each security

in the portfolio at its

end-of-day market price

plus the accrued interest

(less taxes and fund expenses)

For

example:

• Take a portfolio

made up of two bonds:

o BOND

A maturing in 28 years

o BOND

B maturing in 8 years

• Both are purchased

on Jan. 1, 2005 at $103.

• Suppose that on

Nov. 5, 2005:

o BOND

A has a market price of

$114, with accrued interest

of $10

o BOND

B has a market price of

$106 and accrued interest

of $8.

•

Under the accrual method,

you would take the purchase

cost of each:

o $103

for BOND A and $103 for

BOND B

o and

simply add the accrued

interest for a total NAV

of $224 (224=103+103+10+8).

•

Under the marked-to-market

method, you must use current

market prices

o $114

for BOND A and $106 for

BOND B

o And

again add accrued interest

to give a NAV of $238

(238=114+106+10+8).

MTM

accounts for all gains

and losses of the assets

of the Fund on a daily basis. Thus, it reflects

the actual net worth of

the Fund

1. |

when the market

is up, you can realize

the full gains; |

2. |

when the market

is down, you can

buy at market value,

reaping potentially

higher gains than

you would under

accrual valuation

should the market

come back up; and. |

3. |

you know how much

your investment

in the Fund is really

worth, thanks to

a transparent fund

accounting method

that is the convention

for investment-managed

Funds worldwide. |

|

| |

|

| Q. |

How

do I earn from my investment

fund? |

| A. |

Recall that when purchasing

units of participation/shares,

the price of each unit

is determined by the current

day's Net Asset Value.

When redeeming units,

the amount that the investor

shall receive is also

based to the current day's

Net Asset Value. So an

investor can earn on a

UITF when the redemption

price is greater than

the subscription price. |

| |

|

| Q. |

How

can I monitor the fund's

performance? |

| A. |

Prudentialife Optima Funds

sends the following to the

investors:

1. |

Daily Rates. This

is sent to all investors

via e-mail every

morning of a banking

day. This contains

the Net Asset Values

per Unit (for UITF)

and Net Asset Value

per Share (for Mutual

Fund) of the previous

banking day. |

2. |

Daily Update. This

is sent to investors

every afternoon

of a banking day.

This contains the

events explaining

the movements of

the Net Asset Value

Of the previous

banking day. |

3. |

Fund Holdings. This

is sent to all investors

every month and

contains the securities

where the Funds

are invested in. |

4. |

Fund Ranking. This

is sent to all investors

every month and

contains the ranking

of Prudentialife

Optima Funds relative

to similar funds

in the industry. |

5. |

Quarter Reports.

This is sent to

all investors every

quarter and contains

historical financial

information of Prudentialife

Optima Funds as

well as the Investment’s

Manager’s

comments on what

to expect on the

following quarter.

This is sent to

all investors through

mail. |

The above reports can also

be viewed and downloaded

from the website: http://optima.prudentialife.com. |

| |

|

| Q. |

When

does the investment mature?

(No specified tenor - vs.

a fixed tenor of most fixed

income instruments)? |

| A. |

You need to build on the

concept of an "expected

time horizon" for

funds, long term investing/holding

capacity with flexibility

to pay-out.

a. |

For the UITF and

Mutual Funds, no

exact time horizon

exists, but one

can maximize benefits

and minimize risks

of investing in

a fund when staying

medium to long term

(at least 3-5 years). |

b. |

Also, the funds

feature the flexibility

to exit the investment

any time, should

the investor require

to do so. |

|

| |

|

| Q. |

When

would be a good time to

invest? |

| A. |

One can never time the

market; investing should

involve a disciplined

process.

Market Timing is an investment

strategy that seeks to

place the purchase of

investment instruments

on the time that prices

are low so that when prices

go up, the instruments

bought can be sold for

higher prices and thus

the investor can earn

from the sale. The ultimate

goal then for timing the

market is to gain the

maximum return by buying

at the absolute bottom

of the instrument's price

and sell at the very peak.

That is why the biggest

fear of investors is to

enter the market is when

prices are high and expected

returns are lower.

Consider three investors

John, Jack, and Joe, who

invest in a fund invested

in US Dollar denominated

fixed income bonds issued

by the Philippine government.

Suppose now that each

of the investor buys $5,000

to invest at the start

of each year for 10 years;

the only difference is

the time that each investor

enters the market. John

times the market perfectly

and enters the market

at its bottom, i.e. when

prices are low. Jack meanwhile,

is a periodic investor

who places his investment

on the first business

day of the year. Lastly,

Joe times the market in

the worst possible way

and invests at the peak

of the market, i.e. the

prices are high.

The

following table shows

the investment transactions

and the returns for each

year of each investor.

| |

| |

John's Investment |

(Lowest of Year) |

|

Jack's Investment |

(Start of Year) |

|

Joe's Investment |

(Highest of Year) |

(Highest of Year) |

| |

|

|

|

|

|

|

|

|

|

| |

Value as of End of Year |

Return YoY |

Price per Share* |

Value as of End of Year |

Return YoY |

Price per Share* |

Value as of End of Year |

Return YoY |

Price per Share* |

|

1991 |

2,107.45 |

7,226.82 |

44.54% |

2,107.45 |

7,226.82 |

44.54% |

3,385.98 |

4,498.00 |

-10.04% |

|

1992 |

2,919.13 |

13,863.13 |

13.38% |

3,046.03 |

13,620.99 |

11.40% |

3,720.03 |

9,571.81 |

0.78% |

|

1993 |

3,287.51 |

30,855.12 |

63.57% |

3,393.35 |

30,201.32 |

62.19% |

5,533.46 |

20,497.56 |

40.67% |

|

1994 |

4,436.02 |

30,721.78 |

-14.32% |

5,503.66 |

29,182.17 |

-17.10% |

5,707.51 |

20,989.63 |

-17.68% |

|

1995 |

4,439.87 |

44,675.45 |

28.07% |

4,562.58 |

42,585.19 |

24.58% |

5,684.20 |

31,149.52 |

19.85% |

|

1996 |

5,684.20 |

61,858.11 |

24.52% |

5,684.20 |

59,285.22 |

24.52% |

7,079.94 |

43,787.58 |

21.13% |

|

1997 |

7,078.22 |

100,196.76 |

49.86% |

7,078.22 |

96,295.94 |

49.86% |

10,607.76 |

70,622.16 |

44.75% |

|

1998 |

10,162.32 |

109,517.72 |

4.11% |

10,607.76 |

105,237.43 |

3.89% |

11,850.41 |

78,019.96 |

3.17% |

|

1999 |

11,020.52 |

138,513.23 |

20.95% |

11,020.52 |

133,336.07 |

20.95% |

13,392.91 |

99,344.30 |

19.66% |

|

2000 |

13,329.71 |

178,418.96 |

24.32% |

13,329.71 |

171,982.60 |

24.32% |

16,653.33 |

128,482.65 |

23.13% |

|

Rate of return (annualized) |

|

|

28.11% |

|

|

24.38% |

|

|

15.85% |

|

* Share

Prices are based on the

Salomon Brothers Brady

Bonds- Phill.

From their investments,

John gets the highest

rate of return while Jack,

who trails only by 0.73%

behind John, receives

the second highest return.

Joe's investment on the

other hand, gives him

15.85% return, which is

the lowest among the three.

In connection to this,

at the end of ten years

John gets the highest

end value which is $178,418

while Jack gets $171,982

,and Joe $128,482.

From the illustration

presented it is clear

that the one who enters

the market at the bottom,

which is John, gains the

most returns from the

investment while the one

who enters at the peak

gains the least (Joe).

Market timing is difficult

to do. The probability

of bad timing is equally

present as a good one.

In addition, a good market

timing gives only a limited

additional return over

the long term. In this

case, John's return is

only 0.73% higher than

Jack's, who doesn't time

the market and does periodic

investment instead |

| |

|

| |

|

|

{kind=link}